Home sales aren’t expected to slow much, if at all, even amid a record coronavirus outbreak. Super-low rates and the growing prospects of the economy gradually returning to normal are likely to keep demand high.

That’s good news for sellers but bad news for prospective home buyers, who are unlikely to get much of a price break in 2021.

Tears, relief, gratitude, and an end to a long, hard road in sight.

On 15th December 2020, Seattle hit a historic milestone as around a dozen health care workers and first responders were vaccinated against Covid-19 in what was the first run of vaccinations.

With a total of 205,069 cases, 12,649 hospitalizations, and 2,953 deaths in Washington state as of 15th Dec 2020, what does the vaccine rollout could mean for the Seattle housing market?

Before we delve into that, let’s see how the housing market fared last month.

Supply down, sales and prices are up

The saga of acute low inventory continued with available inventory dropping by 53.8% compared to the same time last year. On the other hand, brisk sales continue unabated with Closed Sales up by almost 23% on a year on year basis. The lack of inventory is making potential sellers think twice, knowing their search for a new home could be tough.

One indicator of the sales brisk activity is the ratio of pending sales to new listings. November’s 8,584 pending sales outgained the month’s new listings at 6,425 area-wide. This pattern was interrupted this year only in the months of March and April when the stay-at-home orders were in vogue.

Even in our white-hot housing market, savvy High Networth Individuals (HNIs) and investors are lapping up the Cash flow rentals, while taking advantage of the historic low-interest rates.

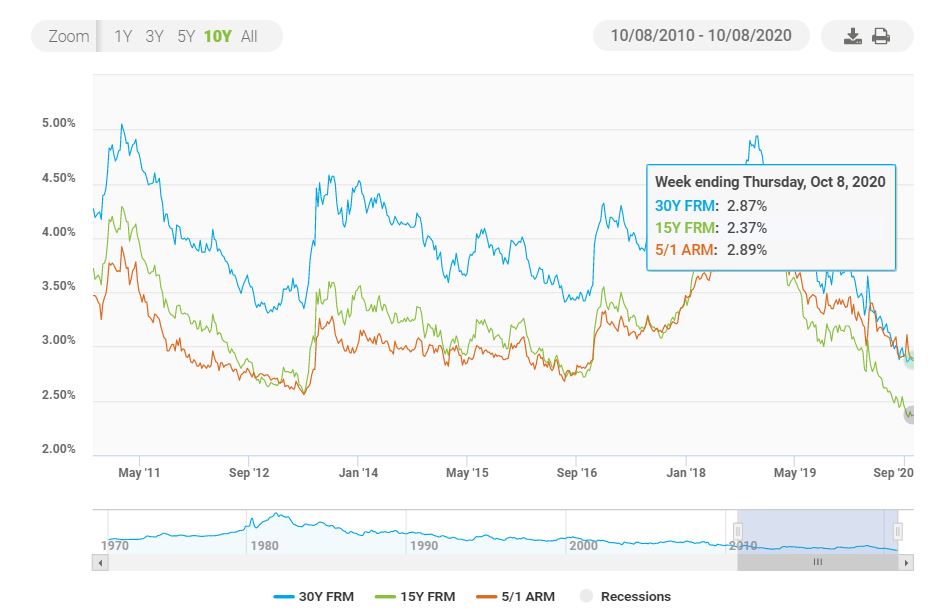

Mortgage interest rates have set record lows more than a dozen times this year, and last week there was yet another. Rates on a 30-year fixed-rate mortgage fell to their lowest level, at 2.71%, for the 14th time this year.

HNI and Millennial Clients driving demand for Real Estate Agents and Loan Officers “Our team has never been so busy with the tremendous demand from the real estate agents and loan officers whose Millennial clients are buying their first home, while their HNIs (High Networth Individual) clients are looking to diversify their portfolio by adding income-producing properties. Of course, the HNIS are looking for a stable asset class vis-à-vis the volatile stocks based investments”, said Vinod Sharma, who is the CEO of www.inBestments.com, USA’s first residential real estate wealth platform that enables the buyers and the homeowners to look at the homes from the prism of wealth, and helps them #BuildWealth with hyper-personalized insights.

COVID-19 vaccine and the Seattle housing market?

COVID-19 has dramatically changed the landscape of the housing market. With low mortgage rates locked-in and a desire for more space amid the pandemic, buyers flooded the housing market in search of bigger homes, away from the crowded urban areas. Now, with vaccine on the horizon, many people are wondering what could it mean for Seattle’s housing market. When “normalcy” begins, whether it’s six months from now, or a year or more from now, what happens to mortgage rates and housing when it returns? No one can be certain but most experts agree there are a few things we can count on.

WFH Trend will continue.

COVID-19 taught us the importance of home and home life. Working from home (WFH) eliminated long commutes and gave us some of our time. Despite all the complications of WFH, buyers are looking for homes with a big backyard and space for a home office. The big tech companies in the Seattle area have already announced plans which allows their employees to continue to work from home in a hybrid model.

People should return to urban areas

Some of the pandemic-driven housing trends with people seeking out larger homes in less dense areas could slow down. People, especially Millenials, will likely return to the urban areas. As the pandemic comes to an end, condos and apartments will see increased activity, sales, and appreciation.

Inventory will increase

Potential sellers who hunkered down to ride out the pandemic could be more willing to host open houses and make a move themselves. This will help alleviate some of our inventory woes.

Foreign buyers return

Before the pandemic hit, there was a significant presence of foreign buyers in our market. A vaccine could also lead to non-US buyers returning to the market, which would increase the buyer demand.

Mortage rates will likely go up

As life gets back to the new normal, people will start spending more, traveling more, eating out more, and doing everything else that stimulates the economy. A stronger economy likely means interest rates may start to rise from our present historic lows.

Next Normal

A safe, effective and widely accessible vaccine would obviously be welcome, but without a crystal ball, it’s hard to know what will happen. Record price appreciation, migration to Zoom towns, and brisk sales certainly weren’t predicted to be an outcome of a pandemic. It will take time for the economy to level out and for people to get back to work, but one thing is certain, we are not going back to the old normal but would rather adjust to the Next normal.

The Federal Housing Finance Agency announced new conforming loan limits for Fannie Mae and Freddie Mac for 2021. The new limit for single-family residential properties is $548,250, which is up nearly 7.5% from 2020’s limit of $510,400 and marks the fifth consecutive year of increases.

All counties in Washington states have increased to the new limit. However, only King, Pierce, and Snohomish counties in Washington are considered “high-cost counties” and have a higher limit of $776,250. High-cost areas have 115% of the local median home value that exceeds the baseline conforming loan limit. Click here to see a map of the new conforming loan limits across the U.S.

In 2016, the FHFA increased the Fannie and Freddie conforming loan limits for the first time in 10 years, and since then, the baseline loan limit has gone up by $131,250.

What does this mean for homebuyers?

Loan limit increases are significant for homebuyers! The increase keeps homebuyers in step with a more expensive housing market like Seattle, by allowing them to borrow more to the limit of what is called a “Conforming Loan”. With conforming loans, buyers can purchase homes with lower down payments and more competitive rates.

Looking to buy true wealth-building homes?

Visit www.inBestments.com, USA’s first residential real estate wealth platform that enables you to buy true wealth-building homes whether you are buying your first home to live in or 60th investment property for cash flow/equity growth.

The volatility surrounding the 2020 presidential election helped push mortgage rates to their 13th record low this year, giving both homeowners and buyers a boost.

“The average 30-year mortgage interest rate fell to 2.72%, an all-time record low. Some 19.4 million homeowners are now in a position to save an average of $309 per month by refinancing, for an aggregate $5.98 billion in potential monthly savings – also the most in history”, said Jo Dixit, who has a unique vantage point being a licensed loan originator and a RE Designated Broker.

With rates now close to a full percentage point lower than they were a year ago, buyers in the 4 county Puget Sound region of King, Pierce, Snohomish, and Kitsap, are snapping homes up almost as fast as they’re listed.

So, last month saw more of the same – unprecedented low inventory, anxious buyers, bidding, and another surge in home prices.

Seattle housing market continued to defy seasonality as new records were broken by both buyers and sellers.

Sellers continued to have little competition as escalation clauses, appraisal gap waivers, and “as-is” offers were used by the buyers fighting hard, to secure a place they could call home.

October 2020 saw a 53.76% drop in active listings compared to the same month a year ago, an increase of 6.2%% in pending sales (mutually accepted offers). On a month-on-month (MoM) basis, the housing supply decreased by 10%.

Sellers are trying to take advantage of the soaring prices as evidenced by the 24.2% increase in New Listings. However, the tremendous pent-up demand aided by the buyer’s desire for a larger home and historic low-interest rates is leading to listings being stripped from the market at a stunning pace.

“Homeowners are saving big by refinancing and are taking advantage of low-interest rates to buy investment properties and second homes. Even in this white-hot, multiple-bid market, there are plenty of cash flowing rental properties available that pay for themselves.

“Smart homeowners are tapping their home equity to grab these income-producing properties”, said Jo Dixit, Designated Broker of BricksFolios Real Estate Solutions, a niche wealth-focused brokerage that enables home buyers to build wealth with smart real estate portfolio.

Find cash flow rentals before your coffee gets cold!

That sum up Pacific Northwest’s housing market in October 2020.

The pandemic has made worse our pre-existing anemic housing supply that has struggled to keep up with the strong demand.

The sharp drop of 43% in supply, a less than one month of supply (0.89), a 50% drop in median Days on Market (6 days), and a whopping 19% surge in prices year-on-year across Western Washington are a testimony to too much demand and inadequate supply.

Homeownership remains the cornerstone of the American Dream. As our living spaces this year turned into offices, schools, and playgrounds, a place to call home is important now more than ever.

“A lot of potential sellers are opting to refinance rather than list, reducing the supply of homes on the market by almost half compared to the same time last year.”, stated Jo Dixit, COO of InBestments.com and the Designated Broker of BricksFolios RE Solutions.

Vinod Sharma, CEO of InBestments.com states that “2020 is set to become a record-breaking year for the housing market thanks to the culmination of 3 factors viz.,

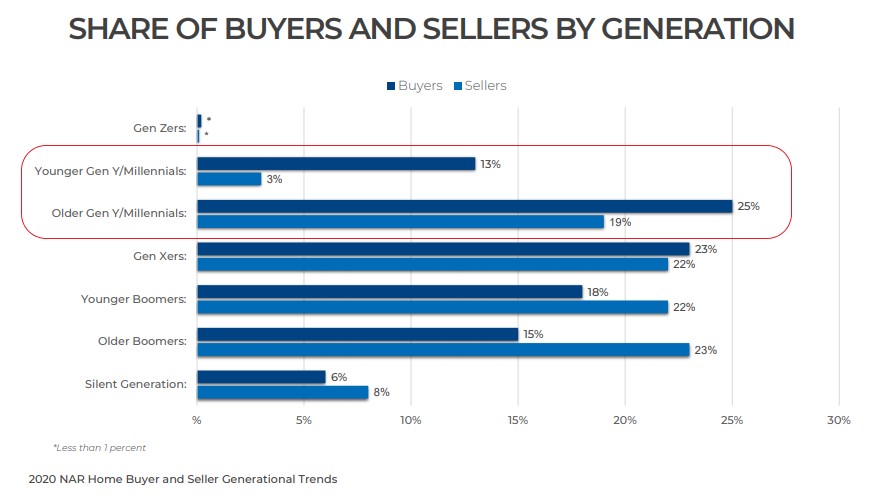

1. Demographics shift with Millennials becoming the largest segment of all home buyers at 38%

Millennials are the largest segment of all home buyers.

2. Historic low mortgage rates are fueling unprecedented refinance activity and driving purchase demand.

If your home loan interest rate is around 3.5% or higher, you could save big by refinancing.

3. The impacts of the coronavirus pandemic. It has lit a fire under buyers who might have been thinking about buying sometime in the near future, but now really NEED to buy.

For instance, the Millennial tech couple with one child in an apartment in Seattle with no outdoor and home office are now desperate for a backyard and larger home. They are willing to move to the suburbs like Lynnwood, Maple Valley, etc., to get it.

It’s a huge multi-year wealth-building opportunity that is just getting started.

Vinod Sharma, CEO of InBestments.com.

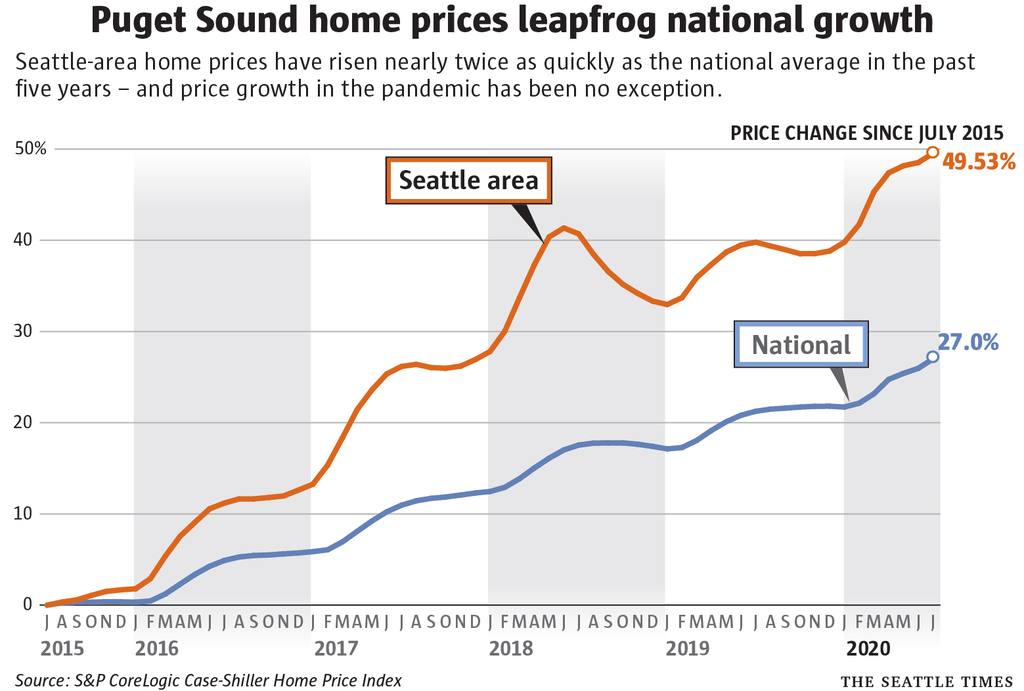

Home prices around Seattle rose faster than in any city in the country, save Phoenix, for the sixth consecutive month. At 49.5% increase prices in our region have risen twice as quickly as the national average in the past 5 years.

Last month saw the largest monthly number of new listings since May 2019. However, supply is extremely anemic at just 1.04 months of supply.

Buyer demand continues to be incredibly strong? with multiple bids becoming a norm.

⚖️The supply/demand imbalance is causing prices to accelerate.

?Median home price in King County has increased by 7.20% while it jumped by 13.4% in Pierce County, by 13.84% in Snohomish County and by 11.84% in Kitsap County.

?Thinking of buying or selling? This is a great time to do it to take advantage of the historic lowest Mortgage rates to buy that dream home or a few cashflow investment properties.

?️Visit www.inbestments.com to get access to true wealth-building homes whether you are buying your first home or 60th investment property for cash flow/equity growth.

")

")