[Updated: 29 July 2022]

The Fed rate has been increased again by .75% on 28th July 2022.

This is not really breaking news but was widely expected given the Fed’s well-published resolve to fight inflation.

The latest increase brings the federal funds rate to between 2.25% and 2.50%, which is where it was at its most recent high in summer 2019 before the coronavirus pandemic.

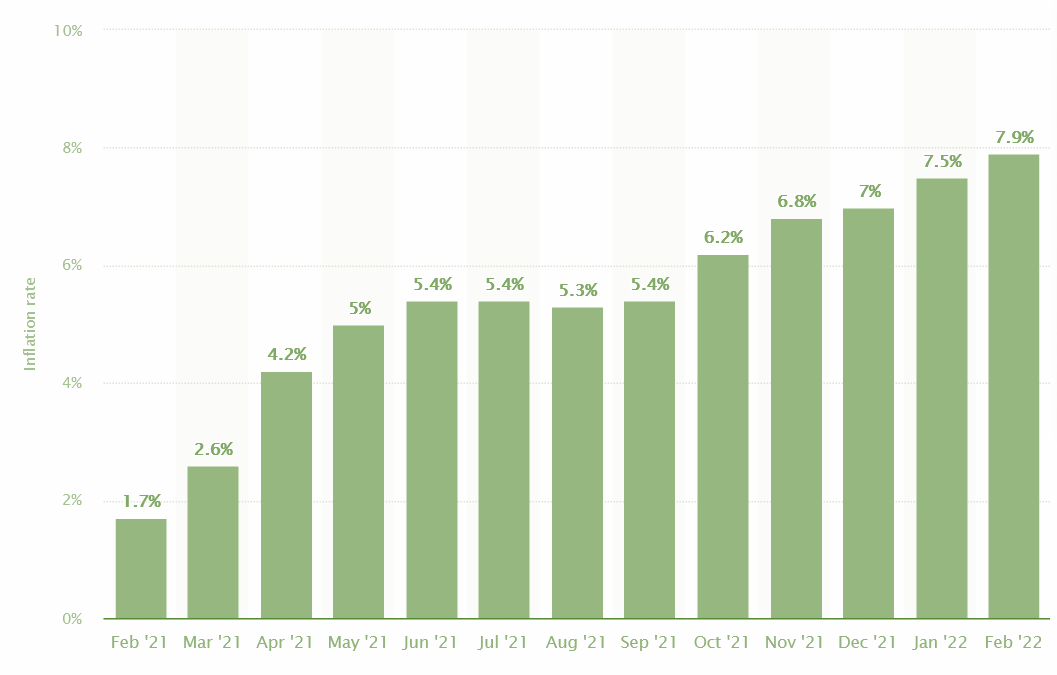

This marks the fourth interest rate hike of the year as consumer prices have risen at the fastest pace in more than 40 years. Five months ago, the federal funds rate was near zero percent.

?Lots of folks are confused between the Fed Rate and the mortgage interest rates.

Fed Rate vs. Mortgage Rates

?♂️The Federal Reserve does not set mortgage rates.

Banks use the Fed rate as a benchmark for what they charge each other for short-term borrowing. However, it feeds directly through to a multitude of consumer debt products, such as adjustable-rate mortgages (when their period is up for adjustment), credit cards, and auto loans.

Fixed-rate mortgages correlate with the 10-year Treasury rate. When this rate goes up, the popular 30-year fixed rate mortgage tends to do the same and vice versa.

The law of supply and demand also influences the rates for fixed mortgages like how the home prices are influenced by the supply and demand for homes. When lenders have too much business, they tend to raise rates to decrease demand and increase the profit. When business is light, they tend to cut rates to attract more customers to increase the volume.

Price inflation pushes on rates as well. When inflation is low, rates trend lower. When inflation picks up, so do fixed mortgage rates.

Are The Mortgage Rates At Historical High?

Reading and listening to the news cycles may make you feel that the sky is falling and the mortgage rates have reached their historical highs, but the fact is they have not.

The mortgage rates are nowhere near their historical highs as can be seen from the chart below from Freddie.

Will people stop buying homes?

Again news cycles may make you wonder like that but let’s see the facts. The chart below shows the Existing Home Sales and the 30-year fixed rate mortgage from Jan 1, 1980.

The average rate for the 30-year fixed-rate mortgage was 5.3% for the week ending Thursday, July 28, 2002, as per Freddie. FYI they publish the weekly average mortgage rates every Thursday.

As can be seen in the chart above, they have been many more years since 1980 when this rate was way higher along with higher home sales.

The highest recorded Existing Home Sales of 7.1 million happened in October 2005 when the 30-year fixed-rate mortgage was 6.07%. We are neither advocating that the present higher mortgage will not have an impact on the demand and are nor trying to imply that these periods are similar. We are merely pointing out that in the past buyers have bought homes with much higher interest rates and their homes still built wealth for them.

Great Investment Opportunites

The combination of blistering home prices for the past 2+ years coupled with the rapid surge in the mortgage rates increased housing inventory, and a record inflation has priced out thousands of potential homebuyers looking to buy a home to live in.

This sudden demand reduction is forcing the builders and the sellers to reduce the prices significantly. The combination of these factors has opened great real estate investment opportunities.

?Savvy investors are taking advantage of this opportunity and are adding great deals to their portfolios. While the regular homebuyer is taking a lopsided view of the surge in the mortgage rates, the real estate investors are taking a holistic look – lower prices, higher rent increase, tax benefits, equity growth, etc.

This opportunity is similar to the one we had at the onset of the pandemic. We at BricksFolios Real Estate Solutions, America’s Real Estate Wealth Advisors, were able to help our investor clients grab some great wealth-building deals at that time.

Watch the video below by BricksFolios co-founder Vinod Sharma to learn how to structure wealth-building deals in any market conditions, including the present high-inflation high mortgage rate market. Learn how smart real estate investments build enduring wealth for you and your loved ones.

Warren Buffett aptly said, “Be Fearful When Others Are Greedy and Greedy When Others Are Fearful.”

✅Get your facts right.

✅Do data-driven smart investments.

✅Don’t let undue fears make you miss the opportunities.

?Book time here for a free consultation to talk about how you can take advantage of this opportunity.

")